English

There are three regulators entrusted with ensuring companies comply with obligations intended to help prevent and track money laundering and terrorist financing under the Anti-Money Laundering and Counter Financing of Terrorism ACT of 2009.

Regulates banks, life insurers and non-bank deposit takers.

Regulates issuers of securities, trustee companies, futures dealers, collective investment schemes, brokers, and financial advisers.

Money changers, non-deposit taking lenders, casinos and any other financial institutions not supervised by the Reserve Bank of New Zealand or the Financial Markets Authority.

As a designated service, you must report certain transactions and suspicious matters to AUSTRAC. Notable ongoing reporting obligations include:

Includes processes and procedures to assist you in identifying, mitigating, and managing money laundering and terrorist financing threats.

Focuses on the procedures for verifying the identities of customers and beneficial owners, including politically exposed persons (PEPs).

There is no such thing as a one-size-fits-all AML/CFT program. Each reporting entity is unique and faces its own set of money laundering and terrorism funding risks. You must design a program that is unique to your needs. This gives you the freedom to choose how to fulfill your responsibilities and to implement stronger and/or additional controls where required.

All AML/CFT Programs must be based on a risk assessment. The risk assessment serves as the basis for your whole AML/CTF program. Your program must explicitly illustrate the relationships between identified risk and the procedures, policies and controls relating to that risk.

You must audit your AML/CFT program (as well as your risk assessment) every two years, or at any time as requested by your AML/CFT supervisor. A copy of your audit may be requested by your supervisor.

It is critical that your auditor has the necessary skills for the role and is independent and not involved in the development of your organisations risk assessment or the creation, execution, or maintenance of your AML/CFT programme.

Designated services should review their AML/CFT program to ensure that:

The program is relevant at all times

Deficiencies in the program's effectiveness are identified

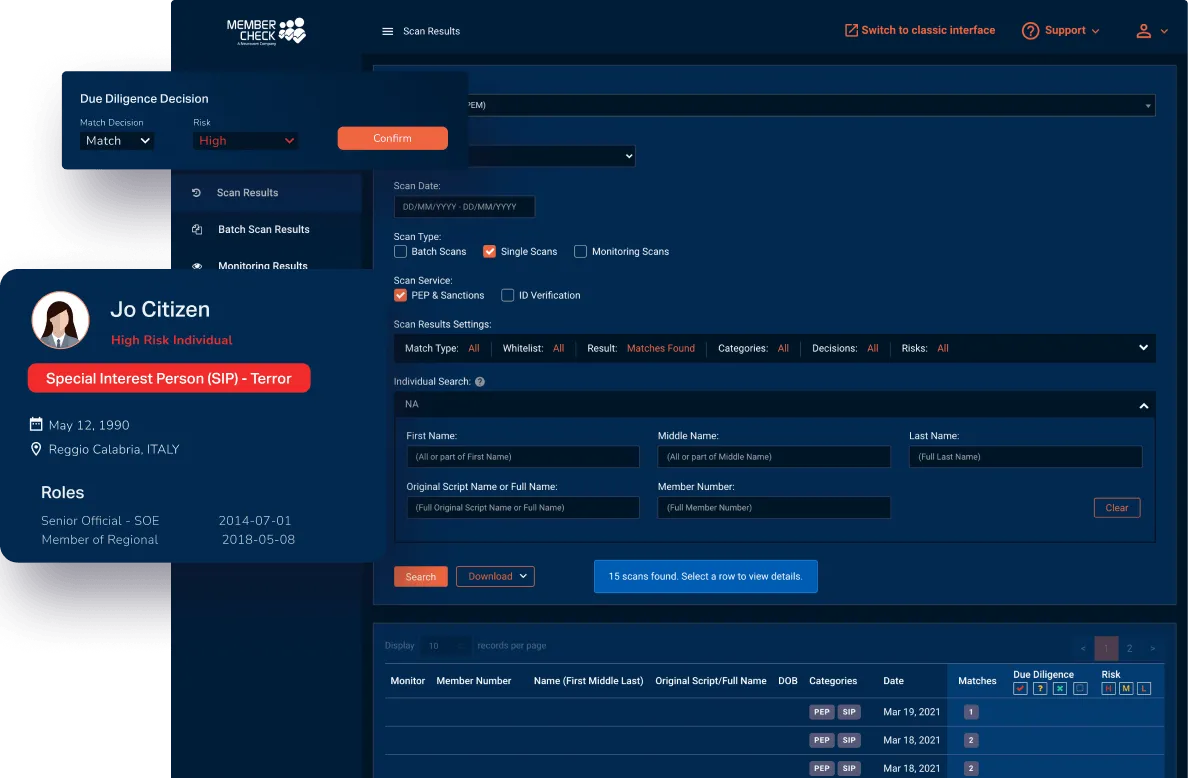

Watchlist Database created using Machine Learning and AI

Our clients are provided with a secure and simple solution in regard to scanning for politically exposed or high-risk individuals, as well as checking names against sanction, regulatory, law enforcement, and other official lists.

Use our sophisticated scan filters and due diligence workflow to minimise the amount of time you spend sorting through, false matches. Scan results and reporting sections allow you to access customer details, whenever and wherever required, as well as download reports, to customise for further investigation or to provide evidence of your AML program compliance for auditing purposes.

* This page is intended as general information only and should not be relied on as the sole source of information for your AML obligations and AML program. Please visit your local regulatory authority sites for the latest relevant and full information.